Converting your LLC to a C Corporation can be a strategic decision that offers potential tax benefits, particularly for businesses aiming to raise capital or qualify for the Qualified Small Business Stock (QSBS) tax exemption. However, the conversion also involves critical tax considerations that must be handled properly to avoid potential pitfalls. This post will walk you through the essential tax steps to convert your business from an LLC to a C corp.

Step 1: Understand the Tax Implications

Before diving into the conversion process, it’s important to understand how an LLC and a C corporation are taxed differently:

- LLC: By default, LLCs are considered pass-through entities. This means the profits and losses of the business pass through to the owners (members) and are taxed at their individual income tax rates. The LLC itself is not taxed unless it opts to be taxed as a corporation.

- C Corporation: C corporations are subject to double taxation, which means the corporation pays taxes on its profits, and shareholders are taxed on dividends they receive. However, C corporations also offer potential tax advantages, such as the Qualified Small Business Stock (QSBS) exclusion and the possibility of deferring taxes by leaving money in the business.

Understanding these tax differences is crucial before moving forward with the conversion.

Step 2: Prepare for Potential Taxable Events

One of the most significant tax considerations to convert an LLC to a C corp is the potential for a taxable event during the conversion. Depending on how the conversion is structured, it may be considered a liquidation of the LLC, which could trigger capital gains taxes for the members.

The following two methods of conversion have different tax consequences:

- Statutory Conversion: This process is available in states that allow direct conversion of an LLC into a C corporation. Generally, this is the most tax-efficient route because the IRS treats it as a nontaxable event under Section 351 of the Internal Revenue Code, which allows the transfer of property to a corporation in exchange for stock without recognizing gains or losses.

- Asset Transfer (Deemed Liquidation): If a direct conversion is not possible, you may need to transfer the LLC’s assets and liabilities to the C corporation in exchange for stock. This can be treated as a taxable liquidation of the LLC, triggering taxes on the appreciated value of the LLC’s assets.

Step 3: Elect the C Corporation Tax Status with the IRS

Once you convert an LLC to a C corp at the state level, you’ll need to notify the IRS of the change in your business’s tax status. This is done by:

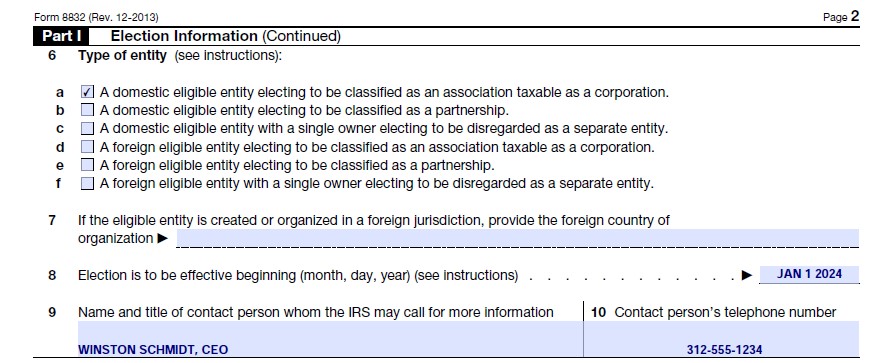

Filing Form 8832 – Entity Classification Election: Use this form to elect to be taxed as a C corporation. You must file this within 12 months of the effective date of the conversion to ensure proper tax classification for the tax year.

2. Apply for a New EIN?: After the conversion, your Corporation may need a new Employer Identification Number (EIN). If your business is the same legal entity and the LLC is simply being taxed as a C corp, you can use the same EIN. However, if a new entity was created, due to a statutory merger, the corporation would need a new EIN. A new EIN can be obtained through the IRS website.

Step 4: Address the LLC’s Final Tax Return

Even though your LLC is converting into a C corporation, you may need to file a final tax return for the LLC. This involves:

Filing the LLC’s Final Return: File your LLC’s final Form 1065 (if taxed as a partnership) or Form 1120-S (if taxed as an S corporation), marking it as the final return. If you have a single-member LLC, there wouldn’t be a final business tax return. Simply, it would be the final Schedule C included on your 1040 tax return at the end of the year. This should cover the LLC’s activities up to the conversion date.

Distributing Remaining Profits: If the LLC has any remaining profits or undistributed earnings before conversion, they should be distributed to members before the conversion. Otherwise, those profits may be subject to double taxation once the C corporation is in effect.

Step 5: Transfer Assets and Liabilities to the C Corporation

For tax purposes, when you transfer the LLC’s assets and liabilities to the C corporation, you’ll need to value these assets properly. Here’s how to handle it:

Valuing Assets and Liabilities: When transferring assets (like real estate, equipment, intellectual property, etc.), ensure they are properly valued. If the LLC’s assets have appreciated in value, this may trigger a taxable event if not structured correctly. Assets transferred in a Section 351 exchange (stock-for-assets) may avoid immediate recognition of gains.

Basis of Assets and Stock: The new C corporation will take a carryover basis in the assets transferred, meaning the tax basis of the LLC’s assets remains the same for the C corporation. However, if the transaction triggers capital gains taxes, the stock received in the new C corporation will have a higher basis.